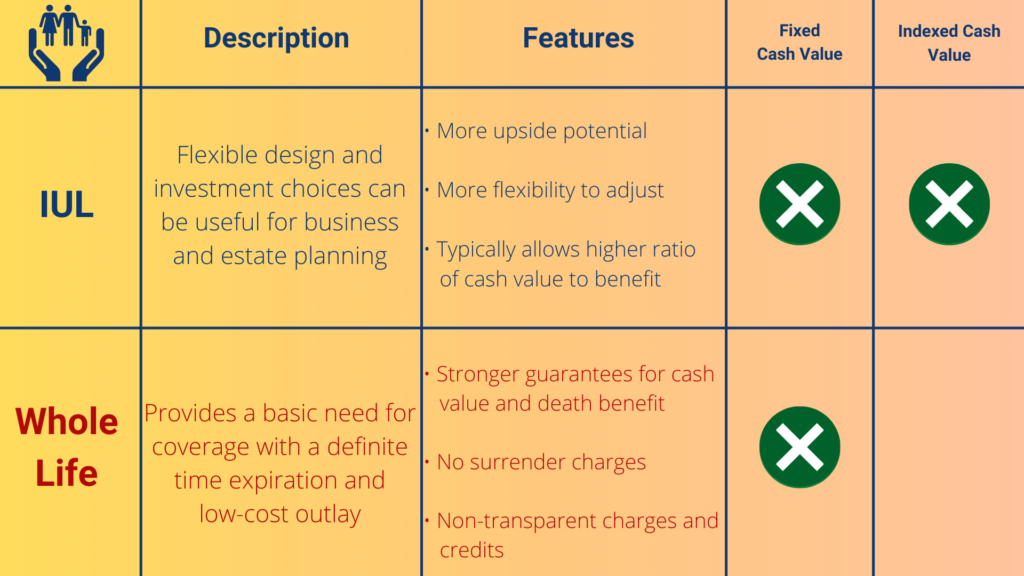

The Real Benefits of Whole Life Insurance: What You Need to Know

Whole life insurance is not just a financial product, but a solid investment strategy that can provide lasting security for you and your family. One of the real benefits of whole life insurance is its cash value component, which grows over time and can be borrowed against, making it a valuable asset for unexpected expenses, such as medical bills or home repairs. Additionally, the death benefit offers peace of mind, ensuring that your loved ones have financial support even after you're gone. This can be particularly crucial for families relying on a primary income earner.

Another significant advantage of whole life insurance is its permanent coverage. Unlike term life insurance, which expires after a set period, whole life policies last for your entire lifetime as long as premiums are paid. This guarantees that your beneficiaries will receive a death benefit whenever you pass away, making it an excellent choice for long-term family financial planning. Furthermore, many whole life policies come with dividend payments, which can enhance the policy's value and provide additional financial flexibility. By understanding these benefits, you can make an informed decision about whether whole life insurance aligns with your financial goals.

Is Whole Life Insurance Worth the Investment? A Deep Dive

Whole life insurance is often hailed as a reliable financial tool, offering both death benefits and a cash value component. Unlike term life insurance, which merely covers you for a specific period, whole life insurance provides lifelong coverage, ensuring that your beneficiaries receive a payout regardless of when you pass away. In addition to the peace of mind it brings, the cash value accumulates at a guaranteed rate, providing potential access to loans and withdrawals. However, potential policyholders should be aware that these benefits come with higher premiums compared to term policies. According to Investopedia, understanding the intricacies of whole life insurance can help you decide if it aligns with your financial goals.

The investment value of whole life insurance should not be taken lightly. Many financial experts argue that while it serves a purpose, it may not be the best option for everyone. The return on investment is often lower than other investment vehicles such as stocks and bonds, primarily due to the high fees associated with policy maintenance and management. A balanced financial portfolio may benefit more from diversifying investments rather than locking funds into a whole life policy. For deeper insights into this topic, check out NerdWallet which explores the implications of investing in whole life insurance as part of a broader financial strategy.

How Does Whole Life Insurance Compare to Term Insurance?

When considering life insurance options, it's essential to understand the key differences between whole life insurance and term insurance. Whole life insurance offers coverage for the policyholder's entire lifetime, provided premiums are paid. This type of insurance also comes with a cash value component, which grows over time and can be borrowed against or withdrawn. In contrast, term insurance only provides coverage for a specified period, such as 10, 20, or 30 years. If the insured passes away during this term, a death benefit is paid to the beneficiaries, but there is no cash value accumulation. For a more in-depth understanding of these differences, visit Investopedia for a comprehensive overview.

Another critical factor to consider is the cost. Whole life insurance tends to be significantly more expensive than term insurance because of its lifelong coverage and cash value component. While term insurance may seem more affordable in the short term, it's essential to keep in mind that it does not build equity. For those seeking lower initial premiums and who need coverage for a temporary period, term insurance might be the better option. However, individuals looking for lifelong coverage and an investment-like growth of cash value may find whole life insurance a more suitable choice. To explore this topic further, check out the article on NerdWallet.